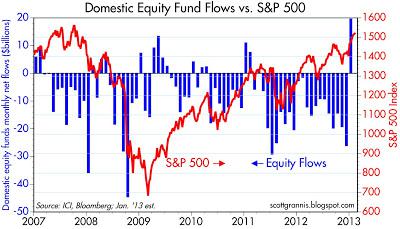

It is imperative to look at the US markets when we are trying to predict global sentiment. More so now as a lot of the quantitative easing for the past 3 years have been sitting mainly by the sidelines, in money market funds and bonds. Somehow, there is a congruence of factors aligning together over the 2 months. First, you have the definitive sustained easing by Federal Reserve until unemployment reaches 6.5%, which won't be likely to be achieved for at least another 6 months. Secondly, you have Draghi somehow pulling a rabbit out of thin air to revive the Euro and that brought about an important demand for the weaker country bonds, which is so crucial in the continuing restructuring and repairing of the EU from the financial mess. Thirdly, you finally have a significant change in government in Abe for Japan, someone who is firmly for a sustained easing policy, targeting an inflation rate of 2%. A new BOJ top gun will be appointed to ensure that target.

The 3 factors all helped to move funds into equity because its pointless to stay sidelined in a near zero interest rate environment. Funds seeking safe havens in the yen and other selected currencies such as Swiss franc have finally turned the other way as they do not see a need for that anymore. Now you have the carry trade going into high gear again - previously the carry trade was in yen based on the near zero interest rate, now the carry trade is also in yen but on the platform that you will be probably be paying back in a weaker yen 6 to 12 month down the road.

US Funds Flow Into Equity

VIX which measures market risk is in a very stable low risk zone.

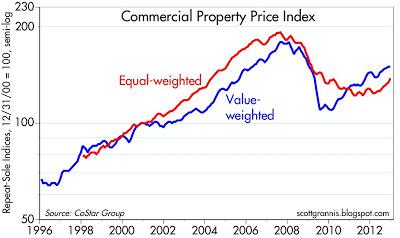

Commercial Property Recovery

0 comments:

Post a Comment